The story of enterprise procurement technology is, in many ways, the story of business software itself. In the 1990s, first-generation ERP suites centralized purchasing, invoicing, and vendor data, promising a “single source of truth.”

The early 2000s layered on browser-based catalogs and self-service requisition portals, easing user friction while remaining tied to ERP backbones that often required expensive customization. Cloud-first P2P suites followed in the 2010s, bringing richer analytics, supplier risk dashboards, and category-specific sourcing tools. Through each new innovation and subsequent operational improvement, procurement teams grew more capable and delivered more value to their organizations. Those gains were real—but each new point solution also introduced seams that had to be integrated, reconciled, and governed.

How enterprise procurement teams go about implementing, integrating, and optimizing new technologies became key differentiators of enterprise procurement effectiveness. A set of universally recognized best practices proved durable: strategic sourcing, category management, no-PO-no-pay rules, guided buying, supplier diversity goals, and more recently ESG scoring. No two organizations apply these playbooks in exactly the same way. This is because no two procurement organizations face the exact same mix of technological challenges or possess the same mix of internal moving parts. A heavily regulated pharma company’s change-controlled intake process bears little resemblance to a high-growth SaaS firm’s fast-track purchasing model.

Yet, as ever, this question of how to better leverage procurement technology—of what strategies to deploy, what types of tools to invest in—remains of crucial competitive importance for procurement leaders. And until very recently, the answers have tended not to be obvious. Procurement excellence historically has come down less to the successful application of any single proven methodology than to finding ways to balance certain sustaining imperatives, such as creating processes people follow, constructing systems such that they share data seamlessly, and managing for oversight and compliance in a way that scales without stifling innovation. This is challenging work.

Now artificial intelligence and agentic orchestration technology loom as the next tectonic shift. Large language models can extract clauses from thousand- page contracts in seconds; generative agents can draft statements of work or recommend suppliers based on live market data. End-to-end orchestration platforms can help internal enterprise teams automate complex processes across teams and technology environments.

Early adopters point to sizable productivity gains and radically improved stakeholder experiences, while also surfacing new concerns—data privacy, model hallucinations, uncontrolled actions, and the sheer complexity of integrating AI into existing landscapes. Traditional rule-based automation cannot fully capture AI’s upside or contain its risks, but neither can organizations afford to rip out the systems that still cut checks and manage compliance.

This research traces procurement’s technological path from the early days of digitization to today’s AI-infused horizon. It examines the pressuresdriving change and outlines emerging patterns from practitioners.

The pages ahead aim to provide perspective—not prescriptions—so you can chart a course that fits your unique environment while preparing for the decade of AI-powered procurement that lies ahead.

A 360-degree snapshot of procurement leadership

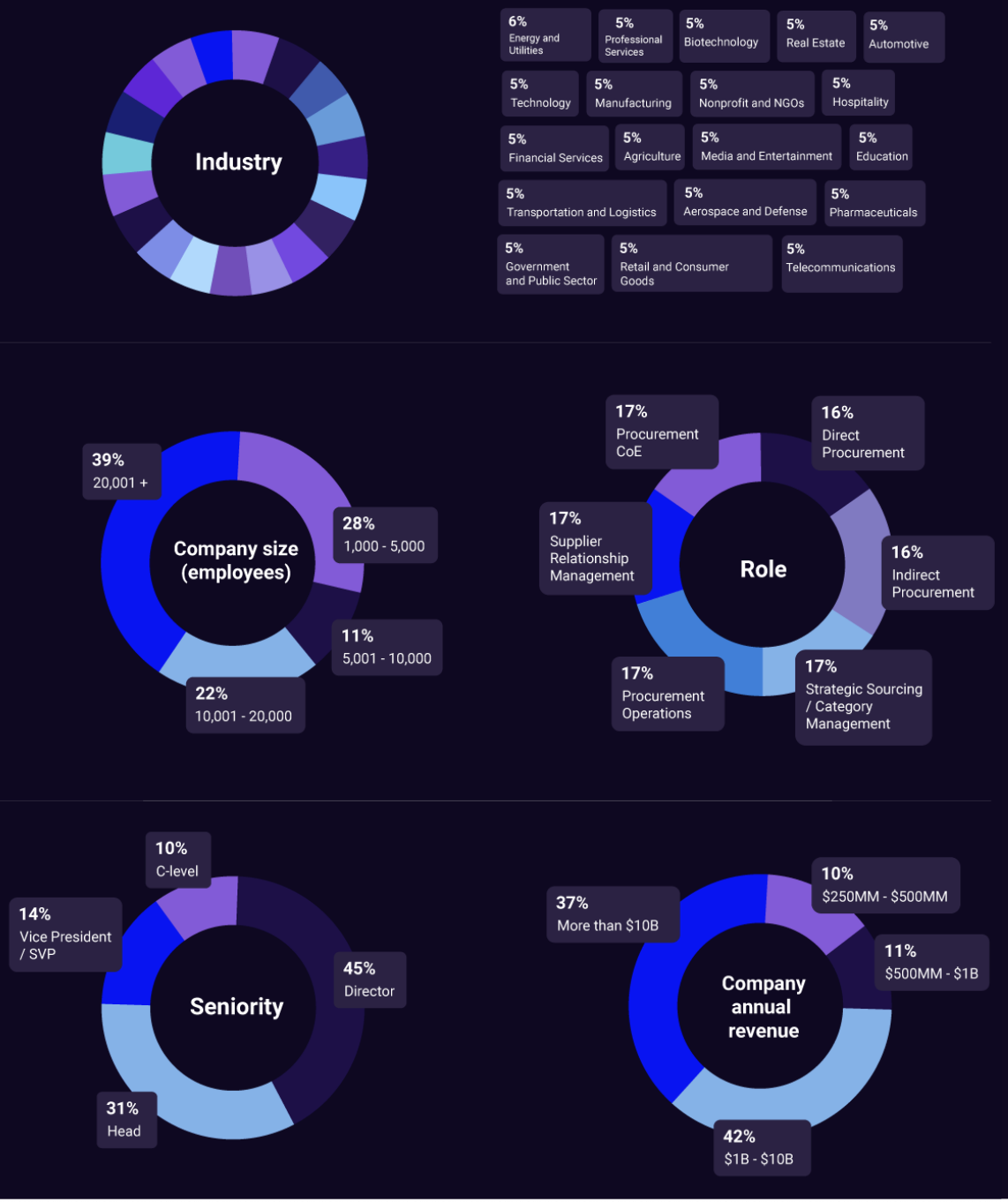

To understand the true state of procurement technology, we partnered with ProcureCon Research to survey 300 senior practitioners in the spring of 2025. Our mixed mode approach—combining online surveys with phone interviews—captured both quantitative data and qualitative insights from procurement leaders worldwide.

The demographics tell a story of comprehensive coverage. Nearly half (45%) are Directors, with another quarter (25%) at VP or C-suite level, ensuring we captured both operational realities and strategic perspectives. Our respondents span organizations from 1,000 to over 20,000 employees, with the largest cohort (38.7%) representing enterprises with 20,000+ employees.

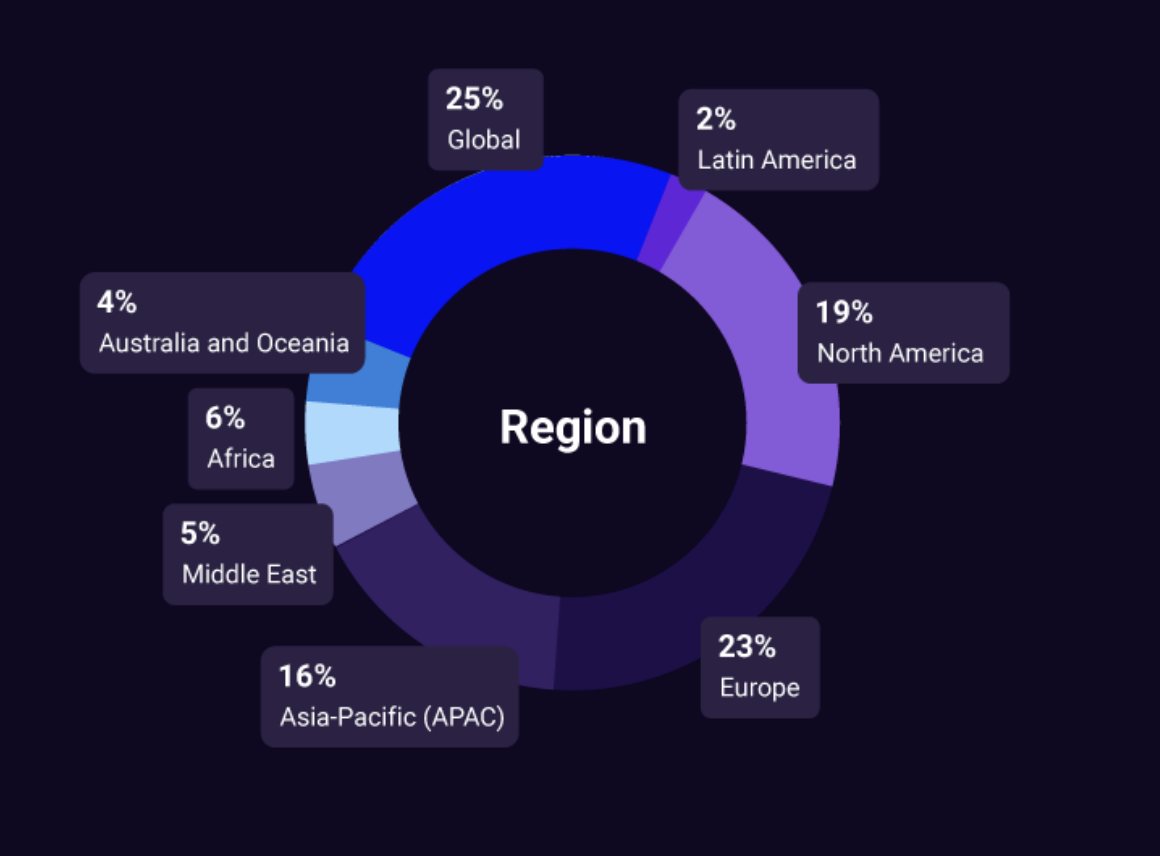

Geographic and industry diversity round out the picture, with representation from 20 industries and strong showings from North America (19.3%), Europe (23.3%), Asia-Pacific (15.7%), and those operating globally (24.3%). This breadth ensures our findings reflect true market conditions, not regional or sector-specific quirks.

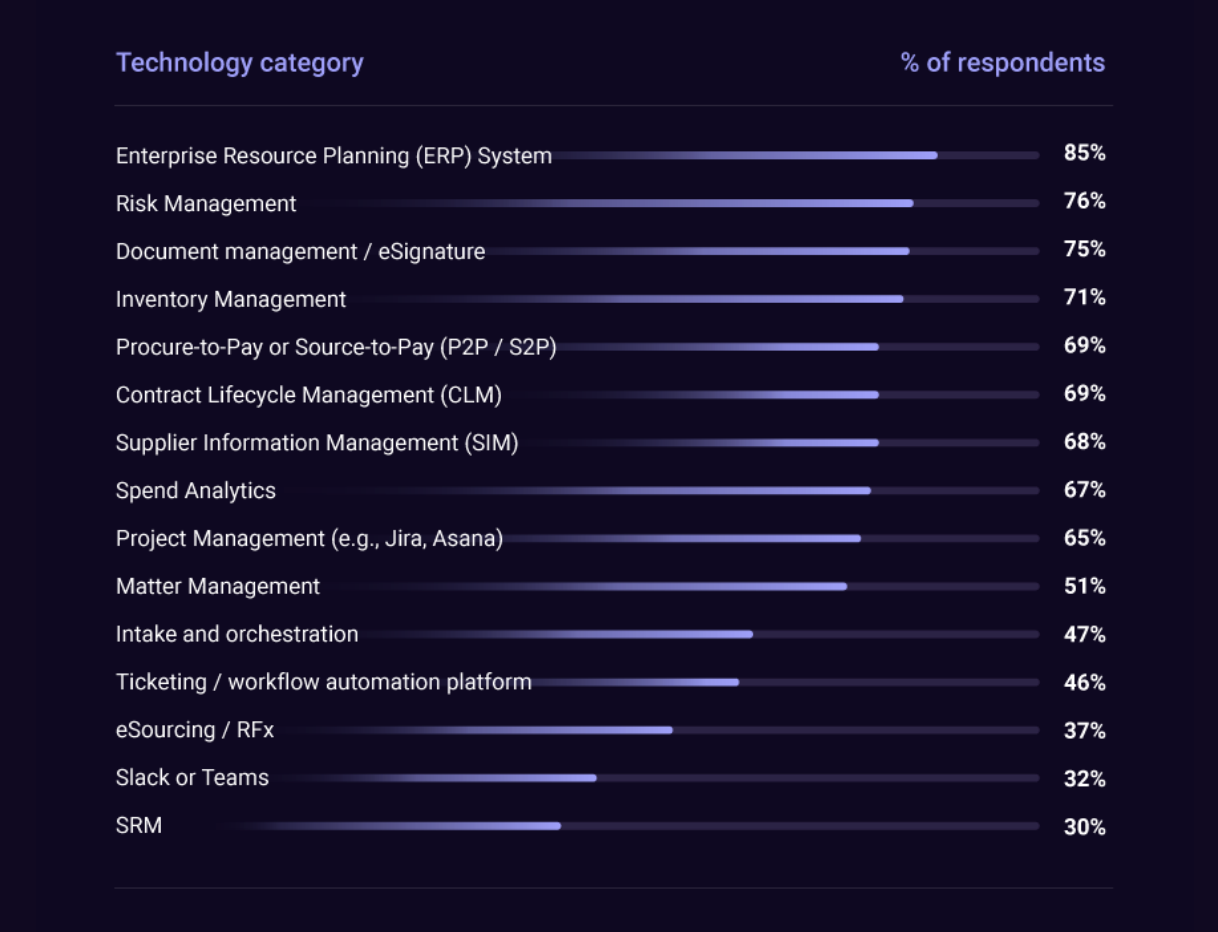

Every function has an app—procurement has 15

Enterprise procurement keeps layering point solutions on top of its ERP “anchor.” The upside is best-in-class capability: specialized sourcing suites, always-on risk engines, AI-powered contract redlining. The downside is a patchwork of logins, data models, and overlapping workflows that no single stakeholder fully sees.

Our 2025 snapshot shows 10 technology categories exceeding 50% penetration—clear evidence that breadth, not breadth-versus-depth, now defines the typical stack. In heavily regulated verticals such as pharma, financial services, and energy, supplier-risk tooling jumps a further 9 percentage points, proving compliance is still the strongest purchase driver.

Implication: The maturity question is no longer “Do you have tool X?” but “How well does tool X talk to tool Y?” As later pages reveal, fragmentation—not functionality—is procurement’s chief bottleneck.

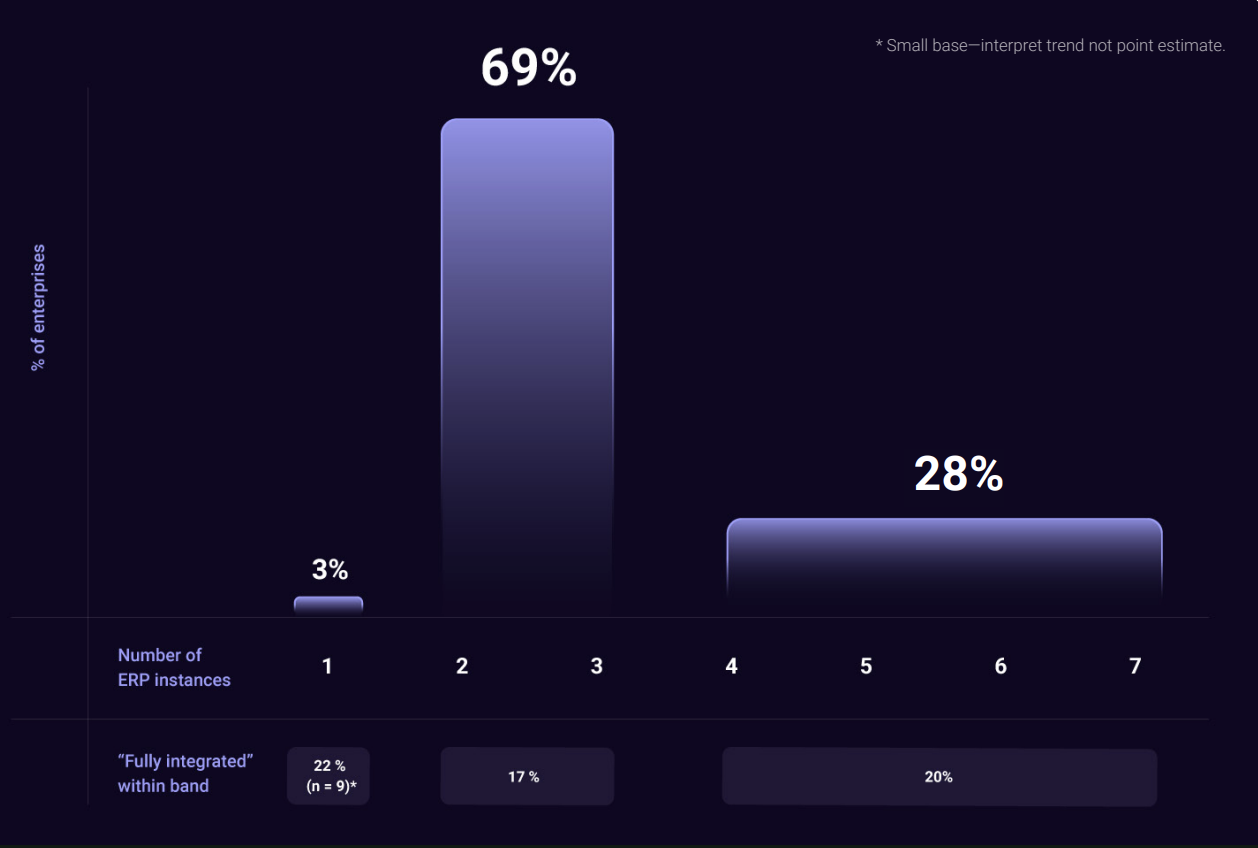

Multiple ERPs are the norm

The phrase “system of record” was perhaps appropriate when one instance of one enterprise resource planning platform truly was the single ledger. M&A, regional decentralization, and business unit carve-outs shattered that ideal. In our survey, 97% of our respondents told us they use more than one ERP, and 28% claimed four or more.

Procure-to-pay and source-to-pay platforms show marginally better consolidation, with 19% of respondents saying they use just one, and 16% using four or more.

Does owning fewer ERPs make life easier? Not according to the data. The share of organizations that call their landscape fully integrated stalls around 20% no matter how many cores they manage. Whether you own one ledger or seven, the API layer still needs stitching; the master-data battle still rages.

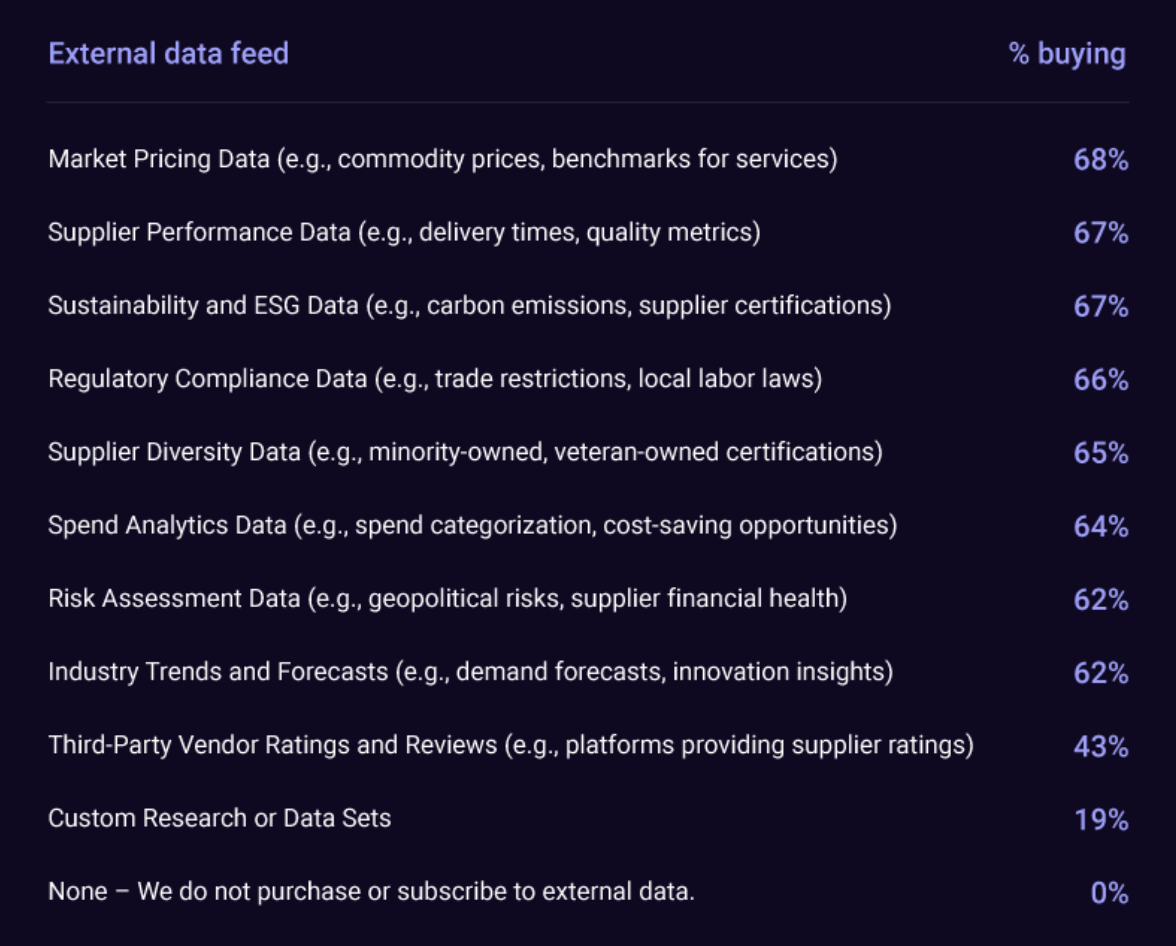

From cost benchmarks to ESG scores, signal flows in from every direction

Not a single survey respondent checked “none” when we asked which external data feeds they purchase. Market pricing, supplier-performance metrics, ESG ratings, regulatory updates—procurement teams are information consumers first and foremost.

The table below shows the 10 most frequently purchased feeds; all but two clear the 60% adoption line. The cross-tabs show that teams operating in heavily regulated industries subscribe to seven more feeds on average than their peers, highlighting how compliance requirements expand the data shopping list.

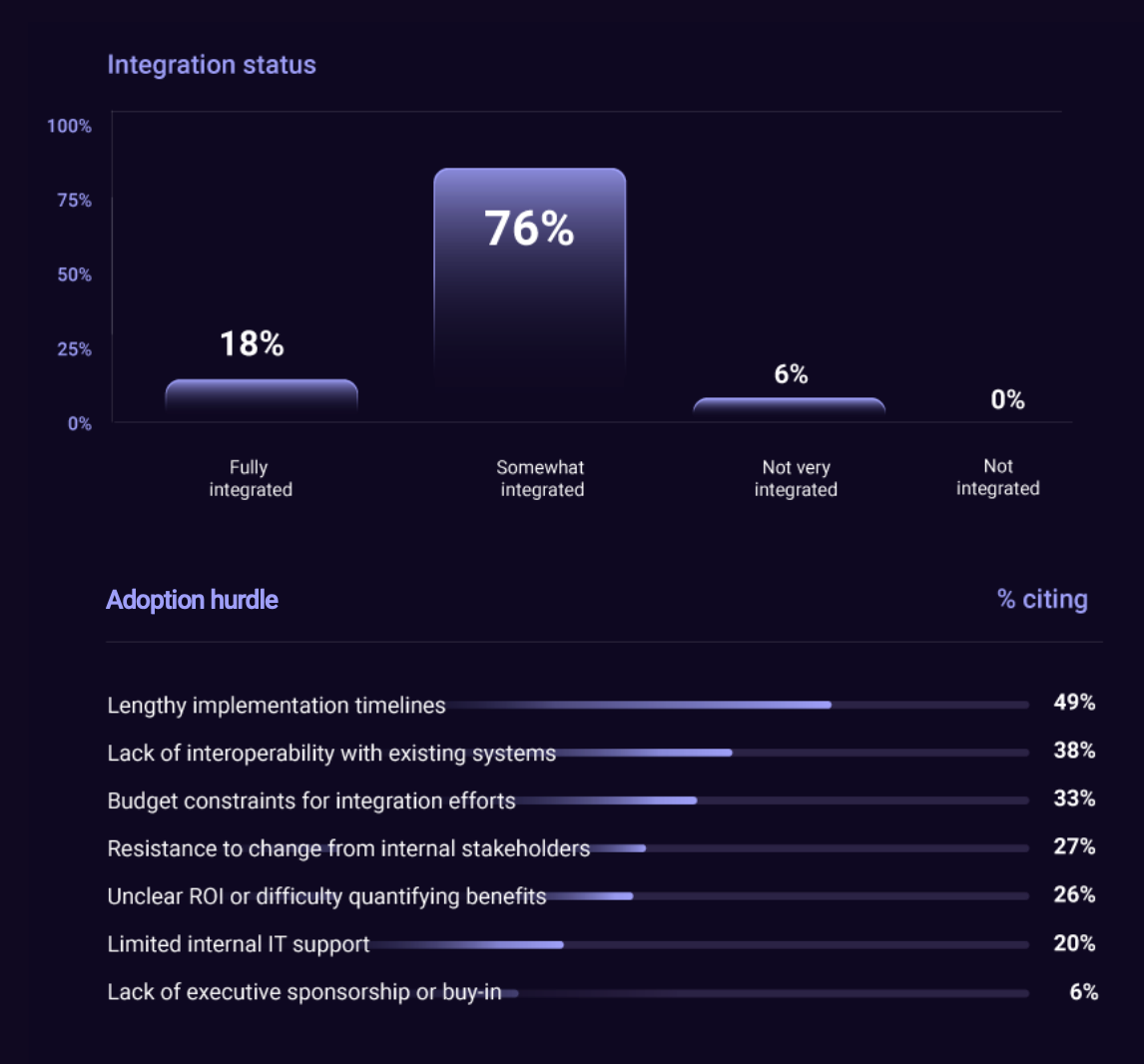

Only one in five stacks “just works”

For all the money spent on point solutions, the connective tissue between them remains thin. Just 18% of leaders label their landscape fully integrated—meaning, for example, that data flows from request-to-pay without swivel-chair work or manual reconciliations. What stands in the way? The answers point to process, not ambition.

Notably and perhaps not surprisingly, respondents whose organizations own an intake and orchestration layer were 47% more likely to say that their tech stack is fully integrated.

Multiple logins, minimal satisfaction

When fragmented tooling meets impatient employees, the user experience collapses: The channel through which a request starts makes a difference. Teams that invite requesters into Slack or Microsoft Teams to initiate requests using plain language more than double the “very satisfied” score—11.8% versus 4.6% for portal-only shops.

Why? A conversational entry point collapses context-switching: the requester stays in their flow while the orchestration layer handles routing, validation, and status updates behind the scenes.

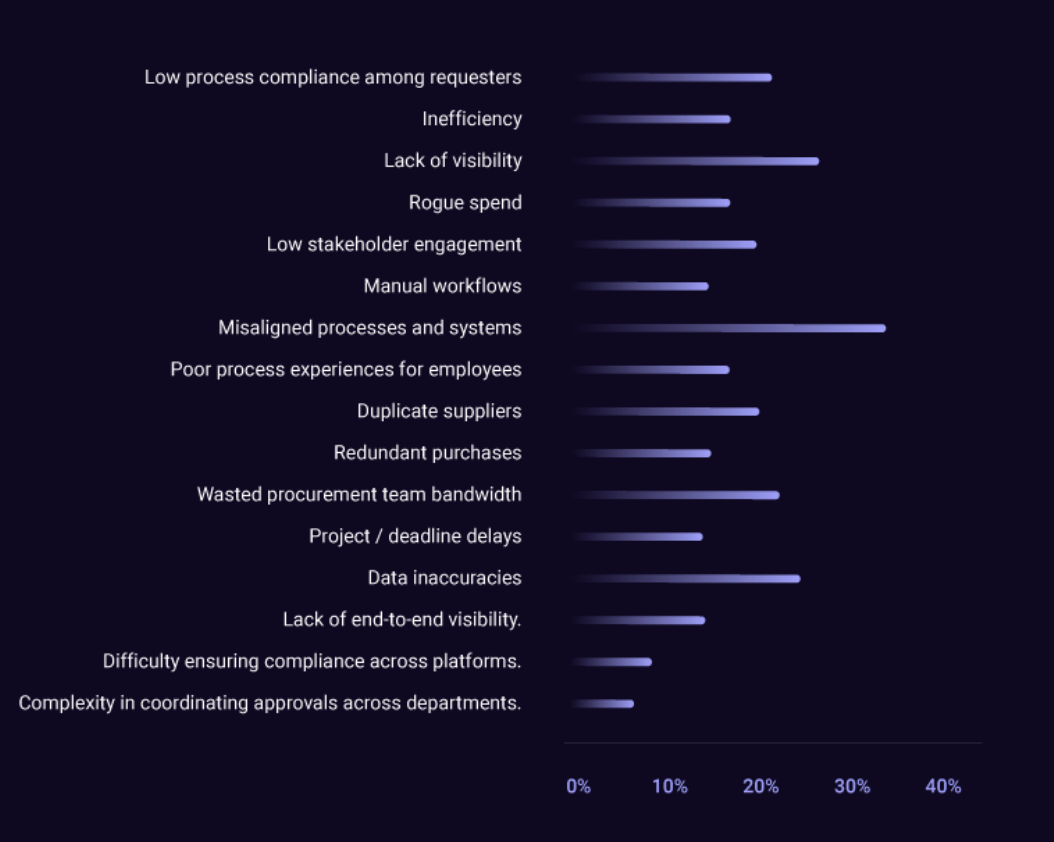

Behind every stalled purchase or rogue invoice is a human frustration.

When we asked respondents to name their top-three pain points, one theme rang loud and clear: mis-alignment—between systems, stakeholders, and the process itself. These frictions don’t just erode efficiency; they sap morale, invite risk, and steal time that could be spent on higher-value work.

Cross-tab spotlight: respondents who described their tool environment as “not very integrated” were 70% more likely to pick “manual workflows” or “inefficiency” as a top frustration than those with fully integrated stacks. In other words, integration gaps translate directly into process pain.

So what? Before layering on more point solutions, leaders should triage these core frictions—simplify intake, unify data flows, connect siloed systems, and surface real time status to requesters. Doing so tackles the big three pains in one shot: alignment, visibility, and compliance.

Compliance lapses ripple through cost, risk, and data quality

We wanted to probe deeper on “low process process compliance among requesters,” since in isolation the problem is somewhat abstract. We asked respondents to select the two most common consequences of poor compliance.

The bottom line? Non-compliant intake isn’t just a nuisance; it’s a triple hit to risk, cost, and clarity—exactly the levers procurement is tasked with controlling.

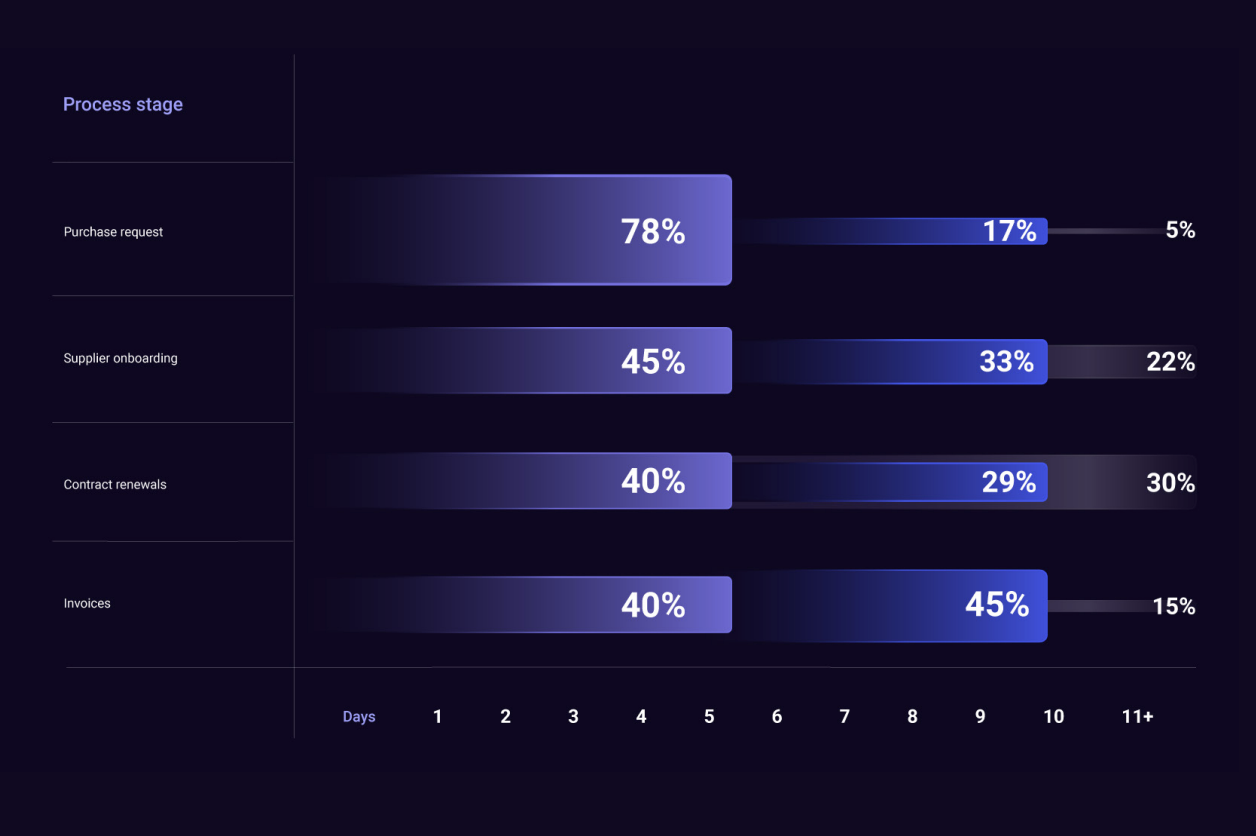

Fast requisitions, sluggish follow-through

Logging a purchase request is the easy part: Seventy-eight percent of organizations turn a requisition into an approved PO in five days or less. After that, momentum fades. When the same leaders clock the rest of the source-to-pay journey, throughput drops by half—or worse.

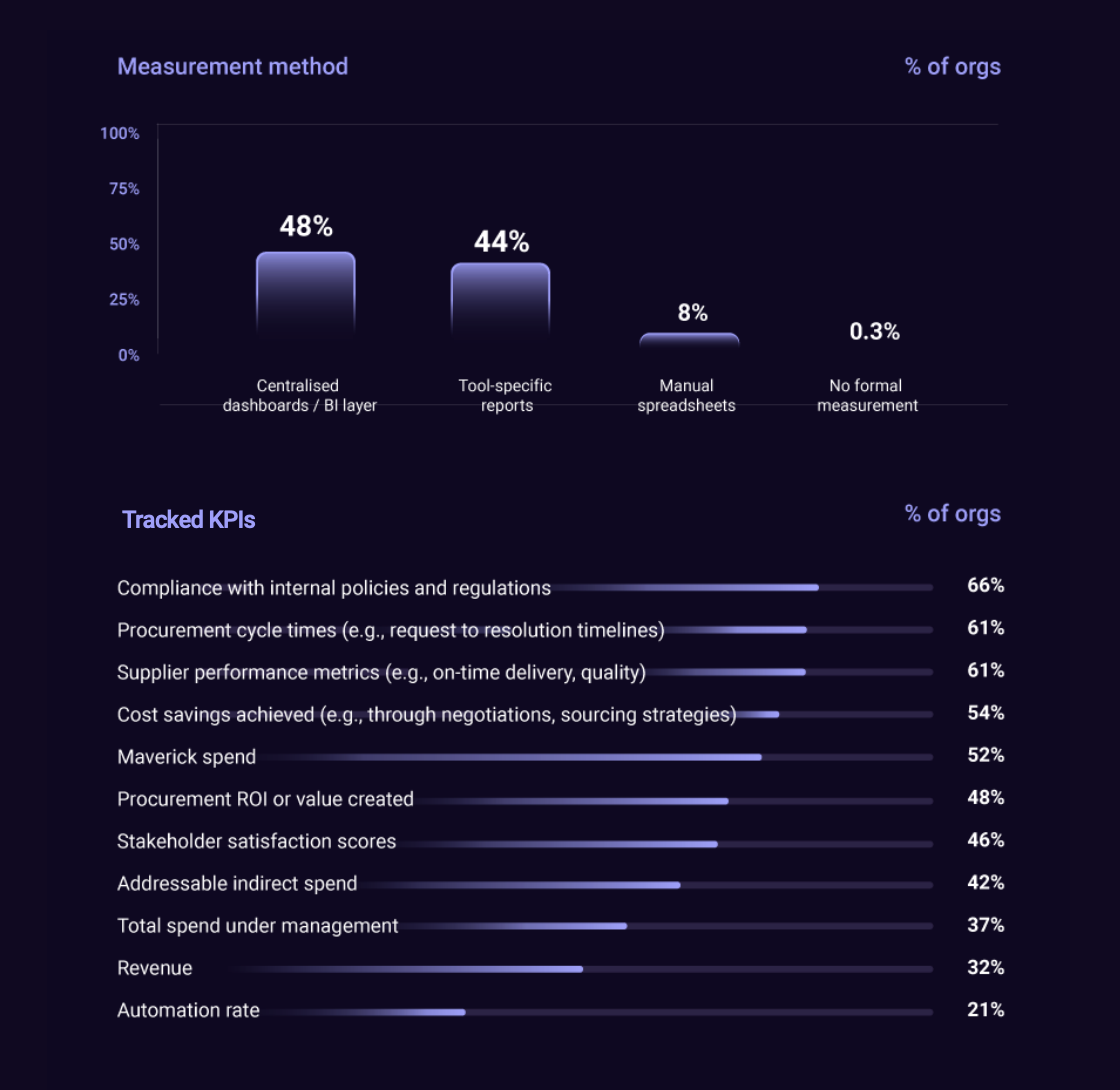

In 2025, procurement isn’t short on metrics; it’s short on accessible metrics. Nearly half of respondents rely on an enterprise data hub or BI layer, yet 44% still pull KPIs from individual point tools. Another 8% admit they build reports in spreadsheets.

What gets measured matters. Risk and speed now rank alongside classic savings targets. Compliance (66%), cycle-time (61%), and supplier performance (61%) form a three-legged stool of “good.” Risk exposure follows at 58%, reflecting geopolitical volatility and ESG scrutiny.

Interestingly, spend under management (49%) falls outside the top three, signaling that leaders know volume alone doesn’t guarantee value.

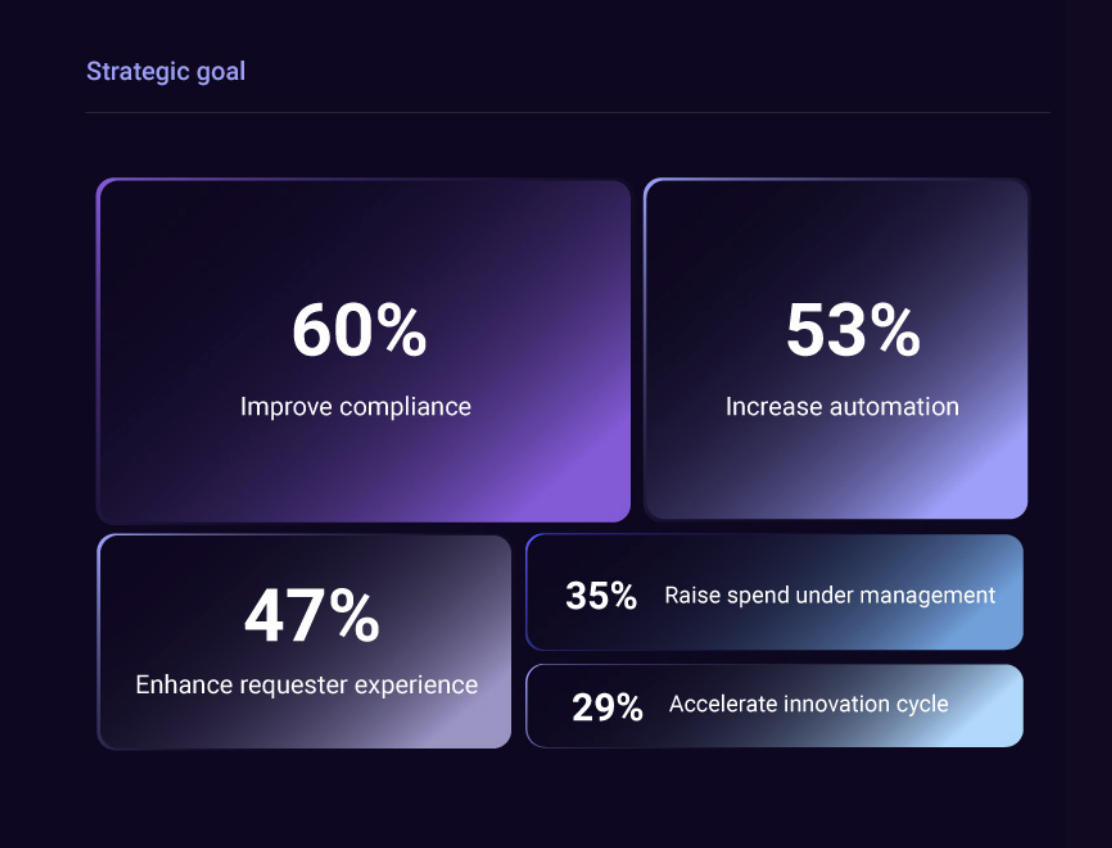

Compliance, automation, experience—then wallet share

Asked to rank their most prominent objectives, respondents deliver a clear hierarchy that mirrors their pain points:

Compliance tops the list because regulators aren’t easing up: ESG audits, supply-chain act disclosures, and data-privacy mandates all land in procurement’s inbox. Automation follows because process staff are drowning in workarounds (see page 7). Experience comes third—leaders recognize that if employees hate the process, they’ll circumvent it, undercutting goal one. Spend under management (SUM) looks modest at 35 %, until you note the baseline: 63% of firms still control only 50–75% of spend through formal channels. Driving SUM north of 80% is hard without fixing intake friction—another breadcrumb pointing toward orchestration investments.

CLM and SRM get the big checks

Budget intent tells an incremental story: big suites don’t vanish; new layers slip in beside them. CLM and SRM dominate because contracts and relationships remain procurement’s fiduciary core. P2P refreshes lag only slightly.

Sub-role cuts reveal nuance. Procurement-Ops teams over-index on P2P refreshes by eight points—they feel the daily grind. Centers of Excellence skew nine points toward analytics and AI—they chase standardization at scale. Together, their investments foreshadow a stack that finally prizes connected processes over another bolt-on portal.

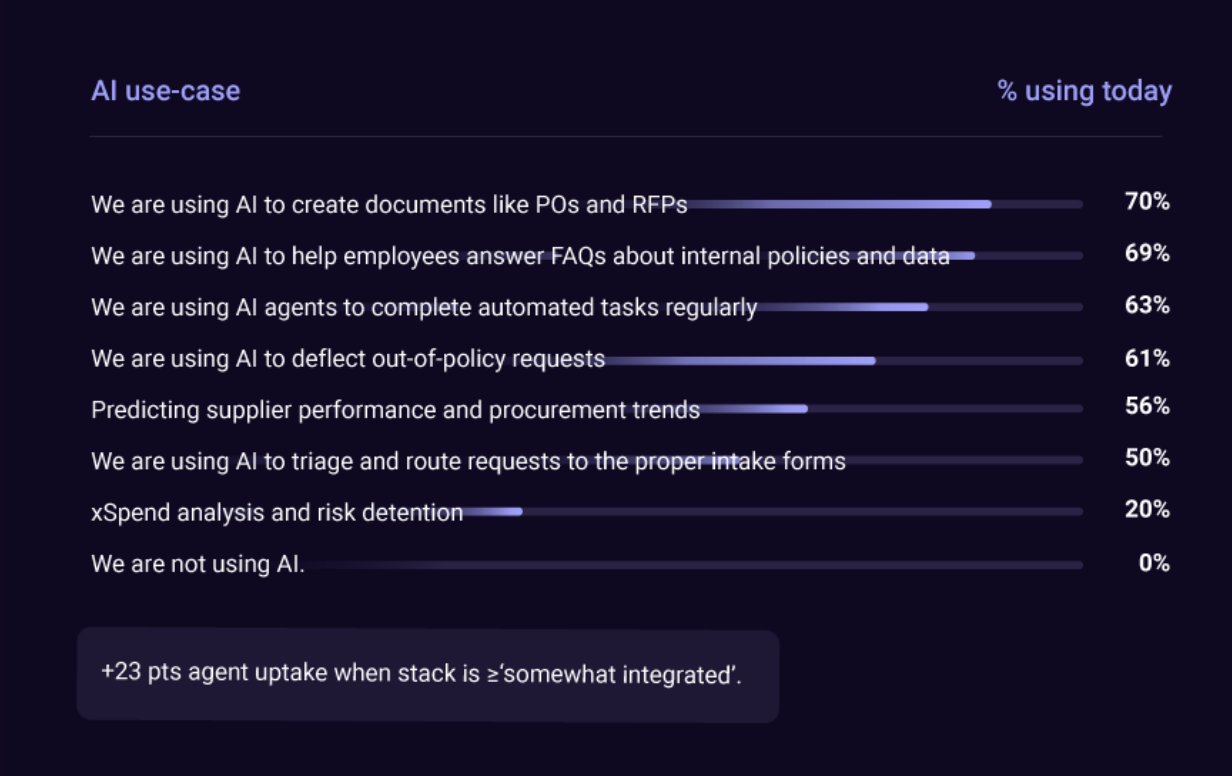

Agents are mainstream—when plumbing permits

The generative-AI debate ended quietly: enterprises adopted first, strategized second. Three of four respondents already generate purchase orders, SOWs, or RFP drafts with an LLM; two-thirds run Slack or Teams bots that answer policy FAQs; 63 % have task-executing AI tools.

Yet adoption is uneven. When we split the sample by self-reported integration level, a pattern emerges: “somewhat-integrated” stacks show a 23-point higher agent usage rate than “loosely integrated” peers. Translation—your AI accelerates only as fast as your connectivity.

Take-away: Early adopters didn’t wait for perfect integration; they piloted where data already flowed. The roadblock isn’t model access— it’s context access.

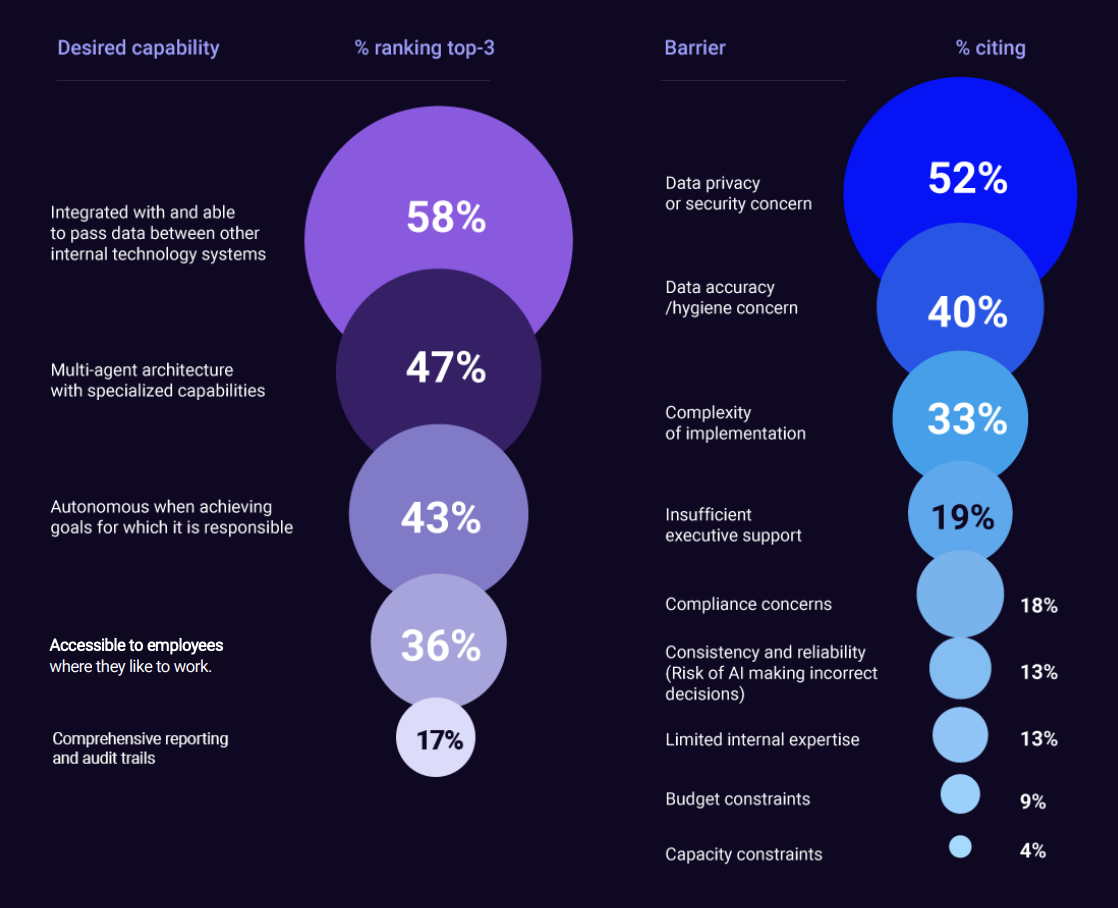

Integration tops the wishlist; privacy and security top the worry list

Having tasted tactical wins, leaders now crave AI that behaves less like a clever assistant and more like a networked colleague. Their top request: agents that talk to every system—58% rank integration as a first- order requirement. Next is multi-agent architecture at 47%, followed by goal-driven autonomy, and then accessibility to employees in their preferred tool at 36%.

Data security and privacy anxiety, meanwhile, outranks all other blockers. Over half the panel fears sensitive data bleeding into public models. Accuracy comes second; ironically, so does integration effort—AI’s promise and peril share the same choke-point.

Orchestration is Step 1 for Enterprise AI

Leaders who plan to expand their intake-orchestration layer next year are 71% likely to rank “AI agents that connect to every system” as a top capability goal. Their peers not prioritizing orchestration post only 48%.

Take-away: Teams see orchestration as the prerequisite layer for trustworthy, cross-stack AI.

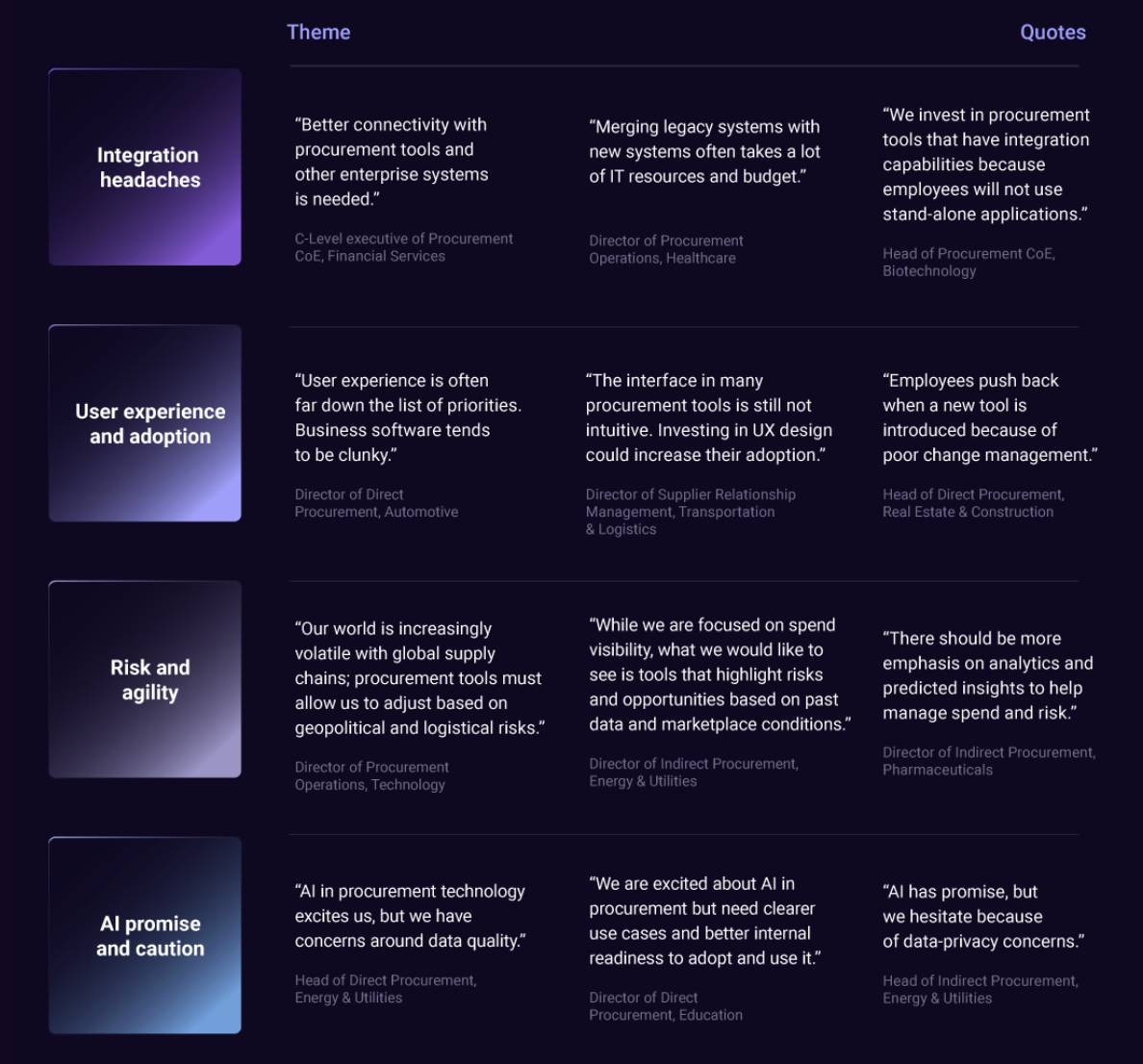

Four refrains from 300 leaders

The survey closed with an open text box—“Anything else you’d like to share about your tech stack?” Two thirds of respondents shared something. We coded every comment into themes and chose representative lines to keep the voice authentic. Every comment points to the same root cause: gaps between great point solutions and the real-world flow of work. When systems don’t talk, people improvise—copy-pasting data, bypassing portals, or delaying decisions until risk is clearer.

Integration headaches lead to clunky user experiences; clunky experiences breed shadow processes; shadow processes erode data quality, which in turn undermines AI and risk analytics. The fix isn’t one more niche tool—it’s a connective layer that unifies data, enforces policy invisibly, and meets employees where they already work.

Fewer seams, richer insight, faster trust.

Connection, not accumulation, will shape the next generation of tech stacks

This survey paints a clear picture of progress and paradox. Procurement leaders have never had so much capability at their fingertips—AI classifiers, risk feeds, contract bots, and specialized suites that cover every subprocess. Yet most still wrestle with slow supplier onboarding, scattered data, and policies that dissolve once work leaves the first screen. The limiting factor is no longer access to technology; it is stitching that technology into a fabric people can follow.

Momentum is already shifting in that direction. Respondents who describe their environments as fully integrated report shorter downstream cycle times and far fewer manual reconciliations. They haven’t jettisoned their existing platforms; they have connected them, wrapped them in user- friendly entry points, and given every data feed a single path into decision-making.

That approach—treating integration and experience as inseparable—marks the next chapter of digital procurement. The challenge is practical, not philosophical: reduce hand-offs, keep requests in one front door, and let information move once instead of many times. Organizations that do so will find that speed, compliance, and insight arrive together, not as separate projects.

The tools are already on the table; the work now is to make them speak the same language.